Positive occupancy trends continue for four straight quarters

The office market in Long Island continues to perform better than the wider United States across several key indicators.

While leasing activity remained relatively subdued throughout 2025, overall absorption — which measures the net difference between occupied and vacated space — stayed positive in every quarter. At the same time, space availability has been gradually decreasing since late 2023.

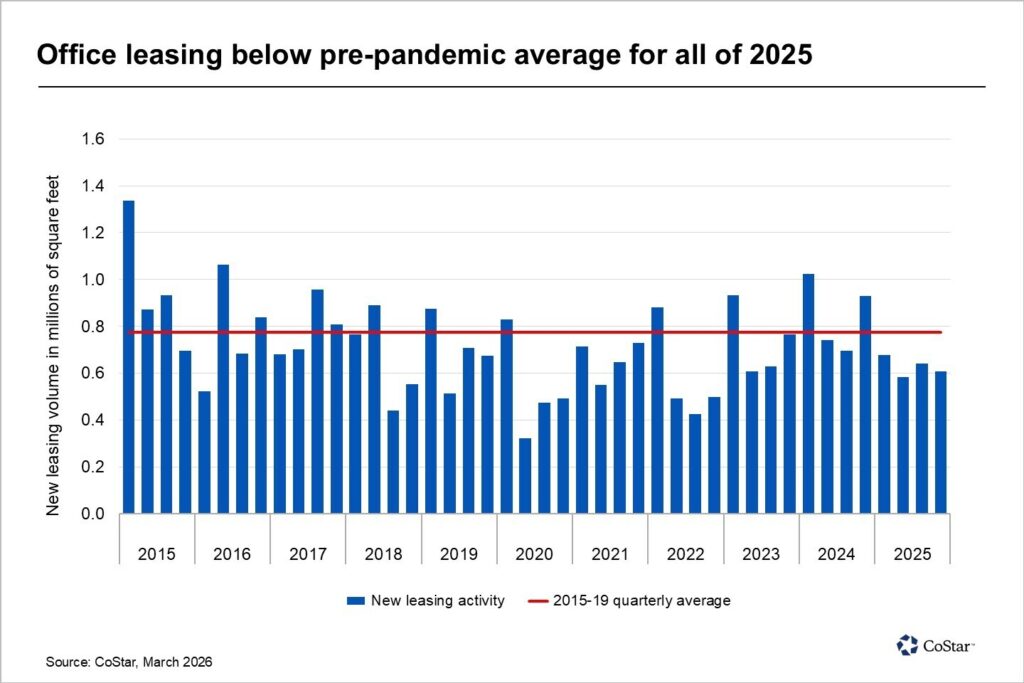

Leasing volumes fell below the five-year pre-pandemic quarterly average for four consecutive quarters. Total leasing activity for 2025 reached 2.5 million square feet, marking the third-lowest annual total in the past decade and representing a 26% decline compared to 2024. This weaker performance was partly due to a lack of large transactions, with no deals exceeding 50,000 square feet during the year.

Despite the slowdown in leasing, net absorption remained strong, totaling 1.1 million square feet by year-end. This made 2025 the first year since 2019 to record positive absorption, as well as the highest annual figure in the past 10 years. A significant portion of this growth — nearly one-third — came from the removal of available space at 200 Jericho Quadrangle, after Northwell Health acquired the 311,000-square-foot site for redevelopment into a healthcare facility.

As a result of consistent positive absorption, Long Island’s office availability rate has been declining since the fourth quarter of 2023, dropping from 11.6% to 8.9% by March 2026. The improvement has been even more noticeable in higher-quality buildings, where availability in four- and five-star properties decreased from 22.1% to 13.2% during the same period.

Overall, Long Island’s availability rate compares favorably with the national average of 15.4%, especially as recovery in the broader office sector has slowed in many parts of the country.

Source: Original reporting by Jared Koeck, CoStar News.