Effective gross income (EGI) is an essential component in real estate analysis, utilized extensively by appraisers, investors, and commercial property professionals. Though the concept is easily grasped, calculating it can be daunting. This guide demystifies EGI and provides practical insights on how to accurately calculate it.

What Is Effective Gross Income?

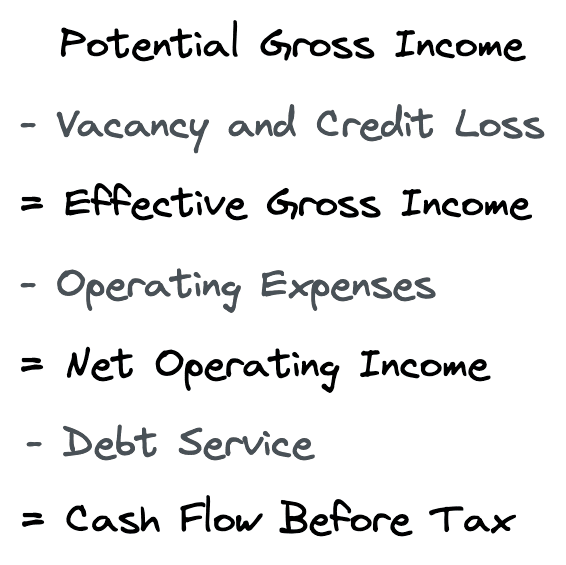

Effective gross income refers to the potential income a property can generate minus losses from vacancies and uncollected rents. It serves as a crucial measure within a real estate proforma, acting as a stepping stone towards understanding a property’s net operating income and cash flow before taxes.

The EGI Formula Explained

The formula for determining effective gross income is fairly straightforward:

Effective Gross Income = Potential Gross Income – Vacancy and Credit Loss

The potential gross income represents the maximum revenue the property can yield if fully occupied, and the deductions account for any anticipated vacancy periods or non-payment of rent. However, as we examine various property types, we note that EGI calculations can become complex due to distinct income sources, lease structures, and market conditions.

This complexity necessitates adaptability in calculations based on property specifics—different types of properties may account for vacancies in diverse ways.

Step-by-Step Calculation of Effective Gross Income

Let’s break down the calculation process using a simple example followed by a more intricate scenario.

1. **Simple Example:** For a single-tenant property with a total potential gross income of $100,000 and a vacancy rate of 10%, the effective gross income calculation would be:

EGI = $100,000 – ($100,000 * 0.10) = $90,000

This calculation is straightforward, and primary vacancies are represented as a single line item.

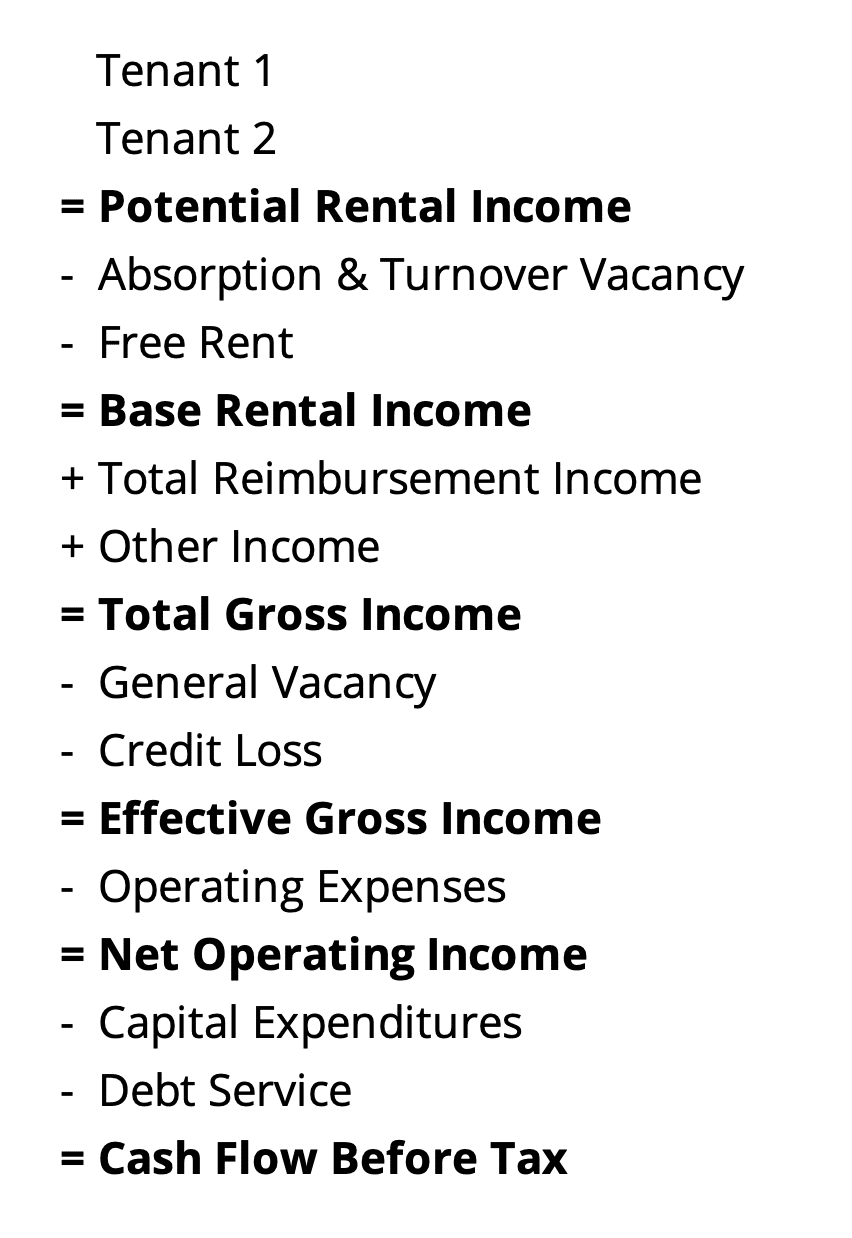

2. **Complex Example:** Considering a multi-tenant office building that’s only partially occupied and experiences varying vacancy rates is more challenging. In such cases, different vacancy categories, including absorption and turnover vacancy rates, must be incorporated. This involves accounting for the time taken for properties to be leased post-occupancy and the time between leases.

A representation of such a proforma might include detailed breakdowns of rents, vacancies, and other income sources, as shown in this image:

Exploring Various Factors in EGI Calculation

Calculating effective gross income effectively necessitates balancing various components, including:

- Base Rental Income: This refers to rent from tenants that landlords can reasonably expect to collect.

- Reimbursement Income: This income can vary significantly based on lease agreements. Under different lease structures such as triple net or gross leases, reimbursement obligations may differ.

- Services Fees: Additional revenue streams, like parking or vending machine income.

After calculating the total gross income with these factors, we must also mitigate for general vacancy factors and any expected credit loss to arrive at the EGI.

Utilizing the Effective Gross Income Multiplier

The effective gross income can be instrumental in determining the gross income multiplier, which helps assess a property’s value. To find this ratio, we divide the sale price by the effective gross income:

EGI Multiplier = Property Sale Price / Effective Gross Income

For instance, if a property sells for $1 million and has an effective gross income of $200,000, the gross income multiplier would be:

EGI Multiplier = $1,000,000 / $200,000 = 5.00

Conclusion

In summary, effective gross income is a vital metric in property financial analysis. Understanding its calculation provides a clearer picture of a property’s financial health.

This guide presented an exploration of the effective gross income formula, step-by-step calculations through both simple and complex examples, and the importance of various factors influencing these calculations. Utilizing the EGI multiplier further underscores its significance in real estate valuation.